In 2024

The judicial system was once again perceived as the main obstacle to the conduct of business activity

The Regional Directorate of Statistics of Madeira (DREM) is today releasing, for the second time, the results for the Autonomous Region of Madeira (ARM) of the Survey on Framework Regulation Costs (Inquérito aos Custos de Contexto – IaCC).

The framework regulation costs may be defined as the negative effects arising from rules, procedures, actions and/or omissions that hinder business activity and are not attributable to the investor, the business itself, or its organisational structure.

The IaCC – referring to the year 2024 – covered nine domains identified as potential areas of constraint on the activity of non-financial enterprises: business start-up, licensing procedures, network industries, financing, judicial system, tax system, administrative burden, barriers to internationalisation and human resources.

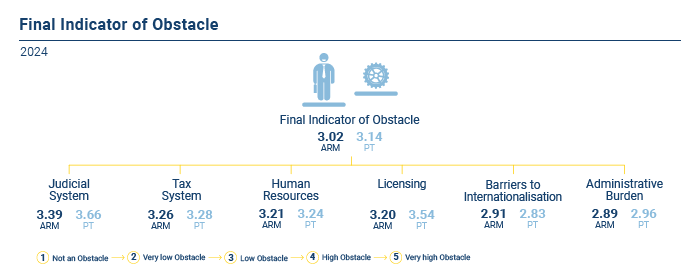

In 2024, the global framework regulation costs indicator for the Autonomous Region of Madeira recorded an intermediate value of 3.02 points (+0.07 compared with 2021) on a scale from 1 to 5, below the 3.14 observed for the country as a whole (3.09 in 2021).

Among the nine domains analysed, the judicial system (3.39), the tax system (3.26) and human resources (3.21) were identified by enterprises as the main obstacles. Licensing procedures and barriers to internationalisation also stand out, with indicators of 3.20 and 2.91, respectively.

Financing was the dimension perceived as posing the least constraint on business activity, both in the Region and nationwide, with values of 2.48 and 2.63, respectively.

With regard to the total costs associated with compliance with information obligations, 81.3% were borne using the enterprise’s own resources (56.2% at the national level), while 18.7% resulted from the subcontracting of third parties (outsourcing) (43.8% nationwide). Registrations and notifications, as well as the provision and submission of business and tax information, accounted for the largest shares of the average annual cost of compliance with information obligations (36.4% and 25.5%, respectively), followed by cooperation with audits, controls and inspections (20.8%).

At the national level, the provision and submission of business and tax information (40.6%) and cooperation with audits, controls and inspections (21.5%) were the components with the greatest weight in the average annual cost of compliance with information obligations.

For more information, please click on: