")

")

")

")

")

")

")

")

")

")

Newsletters

Subscribe to our newsletter and get statistical data as soon as it is available!...

DREM releases information on Framework Regulation Costs for the first time

The Regional Directorate of Statistics of Madeira (DREM) releases today, for the first time, the results for the Autonomous Region of Madeira (ARM) concerning the Survey on Framework Regulation Costs (IaCC).

Although this is already IaCC’s 3rd edition, in previous editions, the sample size for the Autonomous Region of Madeira made impossible the availability of data for the Autonomous Region of Madeira. This situation has now been solved following a request from DREM to Statistics Portugal (INE) - the entity responsible for IaCC at a national level - to enlarge the sample of companies surveyed in the Region, from which 724 valid answers were obtained.

Framework regulation costs may be defined as the negative effects arising from rules, procedures, actions and/or omissions that hinder the activity of companies and that are not attributable to the investor, the business, or the organisation.

IaCC - which refers to the year 2021 - focused on nine domains, identified as potential areas of obstacle to the activity of non-financial companies: opening of activity, licensing, network industries, financing, judicial system, tax system, administrative burden, barriers to internationalisation and human resources.

In 2021

The judicial system was perceived as the greatest obstacle to doing business

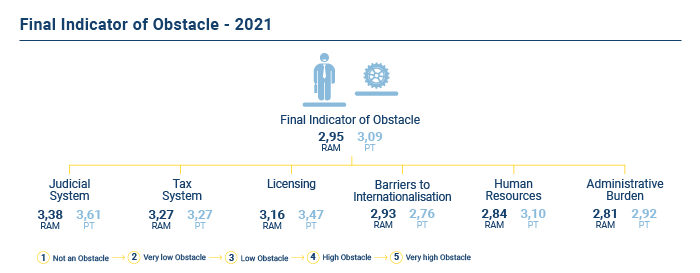

In 2021, the global indicator of framework regulation costs, concerning the Autonomous Region of Madeira, which aggregates nine areas, scored an intermediate value of 2.95 points on a scale of 1 to 5, below the 3.09 registered in Portugal.

Amongst the nine areas under analysis, it was in the judicial system (3.38), the tax system (3.27) and licensing (3.16) that companies identified the greatest obstacles, the same as in the country. Also of note are the barriers to internationalisation and human resources, with indicators of 2.93 and 2.84, respectively.

While in the Region, it was the opening of activity that was perceived as the dimension that represents the least hindrance to company activity, with an indicator of 2.71, the same cannot be said for the country, in which it was financing, with 2.62, the area identified as being the least problematic.

In the set of costs associated with the fulfillment of information obligations, 77.2% was supported by the company's own means (67.9% in the country) and 22.8% was determined by subcontracting third parties (32.1% in the country). Registrations and notifications and cooperation with audits, inspections and checks had the greatest share in the average annual cost of compliance with information obligations (32.8% and 26.5%, respectively), followed by the provision and delivery of business and tax information (22.7%).

In Portugal, the components that recorded the greatest share in the average annual cost of compliance with information obligations were the provision and delivery of business/tax information (43.2%) and cooperation with audits, inspections, and checks (19.2%).

Within the scope of the support measures for companies created in the context of the Covid-19 pandemic, the complexity of adhering to the support measures was perceived by companies in the Autonomous Region of Madeira as a higher obstacle (with an indicator of 3.09) than in Portugal (with an indicator of 2.69). For 11.6% of the companies of Madeira, the complexity of adhering to these measures was even a high or very high obstacle (6.4% in Portugal).

For more information, please click on:

International Statistical Cooperation

|

International Statistical Cooperation

|

Statistical Literacy

|

Statistical Literacy

|

|

|

|

|

|

|

Copyright © 2026 Direção Regional de Estatística da Madeira. All rights reserved.

Address: Calçada de Santa Clara 38, 9004-545 Funchal, Madeira Island

Phone: +351 291 145 126 (National landline call)