")

")

")

")

")

")

")

")

")

")

Newsletters

Subscribe to our newsletter and get statistical data as soon as it is available!...

[NOTE: Due to a column mismatch in the data file—subsequently corrected—the figures relating to deposits held by households and NPISHs were mistakenly interchanged with those of Non-Financial Corporations (NFCs) in the release published on 19 May 2025. The version below has been duly corrected.]

In the 1st quarter of 2025

Loan balances granted to non-financial corporations decreased year-on-year, while those granted to households increase

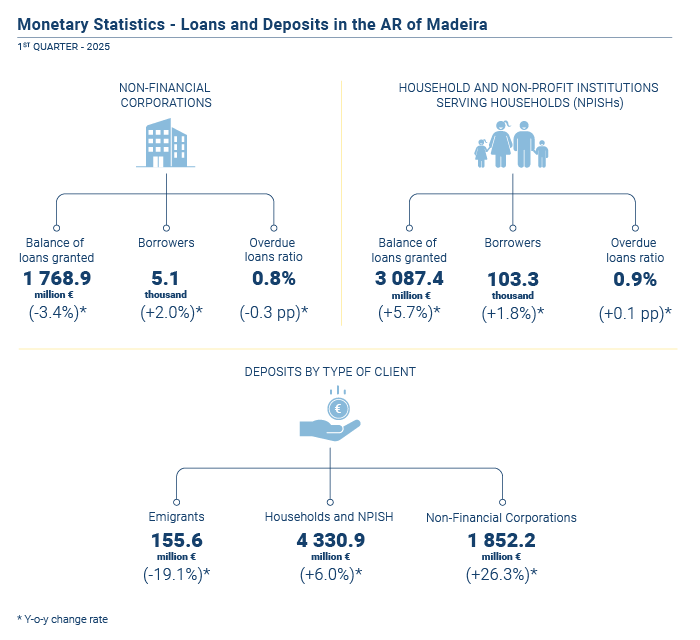

According to data provided by Banco de Portugal, at the end of the 1st quarter of 2025, the outstanding amount of loans granted to non-financial corporations (NFCs) stood at 1.8 billion euros, representing a decrease of 62.6 million euros (-3.4%) compared to the end of March 2024, and a reduction of 0.9 million euros (-0.1%) compared to December 2024.

The non-performing loan (NPL) ratio for this type of corporation increased compared to the end of 2024, rising by 0.1 percentage points (pp) to 0.8% at the end of the reference period. However, in year-on-year terms, there was a decline of 0.3 pp. Nationally, this indicator stood at 1.9% at the end of the 1st quarter of 2025, increasing compared to the previous quarter (+0.1 pp), but decreasing year-on-year (-0.1 pp). The volume of non-performing loans granted to NFCs headquartered in the Region amounted to 14.7 million euros, up by 2.2 million euros compared to December 2024, but down by 4.6 million euros compared with March of the previous year.

The proportion of NFC debtors with non-performing loans stood at 13.5% at the end of March 2025, a figure below the national average (14.1% for the same period). Compared to March 2024, this indicator declined by 0.7 pp in the Region and by 0.4 pp nationally.

In the household and Non-Profit Institutions Serving Households (NPISH) sector, the outstanding balance of loans increased by 167.7 million euros (+5.7%) year-on-year, reaching 3.1 billion euros at the end of the 1st quarter of 2025. Compared to the previous quarter, this represented a growth of approximately 56.1 million euros (+1.9%). A more detailed analysis reveals that 74.5% of the total loan balance was allocated to housing credit, with the remaining 25.5% corresponding to consumption and other purposes.

The overall NPL ratio for this institutional sector was 0.9%, up 0.1 pp year-on-year, but unchanged compared to the end of 2024. The housing segment maintained its historic low of 0.2%, matching the national figure, while the consumption and other purposes segment rose to 2.7%, 0.2 pp above the national level.

Non-performing loans in this sector amounted to 26.6 million euros — of which 5.4 million euros corresponded to housing and 21.3 million euros to consumption and other purposes. Overall, this represents a year-on-year increase of 10.4%

The number of debtors in the household and NPISH sector rose to 103.3 thousand (+1.8 thousand; +1.8%) compared to the same quarter of the previous year. Of these, 42.7 thousand had housing loans (-0.2 thousand; -0.5%), and 87.7 thousand had loans for consumption and other purposes (+1.8 thousand; +2.1%).

The proportion of household and NPISH debtors with non-performing loans in the Autonomous Region of Madeira (ARM) stood at 6.1% at the end of the 1st quarter of 2025, compared to 7.4% in Portugal. These figures remained unchanged from the same quarter of the previous year, both in the Region and nationwide.

DREM resumes publication of Bank Deposit Statistics

From this quarter onwards, the Regional Directorate of Statistics of Madeira (DREM) resumes the dissemination of data concerning bank deposits, broken down by type of client (emigrants, households and NPISHs, and Non-Financial Corporations – NFCs), and by month, beginning with December 2018.

Between the end of 2018 and the end of March 2025, deposits from Households, NFCs and Emigrants followed distinct trajectories, reflecting differing economic dynamics.

NFCs exhibited a generally upward trend in deposits throughout the period, albeit in a non-linear manner. Comparing year-end figures with the corresponding period of the previous year, increases of 10.8% in 2019, 13.1% in 2020 and 19.1% in 2021 were recorded, with the latter representing the highest growth rate of the period. In 2022 and 2023, the pace of growth slowed to 14.4% and 3.8%, respectively. However, in 2024, deposits from NFCs rose markedly once again, registering an increase of 18.6%. By the end of March 2025, NFC deposits had reached their highest level since the beginning of the series, totalling 1 852.2 million euros. Year-on-year and quarter-on-quarter growth rates stood at 26.3% and 6.7%, respectively.

Deposits from households and NPISHs (4 330.9 million euros at the end of March 2025) also displayed an overall upward trend, although more irregular and of lesser magnitude. The change between the end of 2018 and the end of 2019 was minimal (+0.2%), followed by an acceleration in 2020 (+3.3%) and a deceleration in 2021 (+2.6%). In 2022, deposits increased by 7.2%, while in 2023 growth slowed again to +0.5%. In 2024, the most significant annual increase of the period was observed (+7.3%). Year-on-year and quarter-on-quarter increases amounted to 6.0% and 1.0%, respectively.

In contrast to households and NFCs, the evolution of emigrant deposits showed a downward trend throughout the period under review. However, this decline was characterised by alternating phases of acceleration and deceleration, with changes ranging from a maximum decrease of -23.1% in 2019 to a minimum of -9.8% in 2020. At the end of March 2025, emigrant deposit balances stood at 155.6 million euros, representing a 9.5% decrease compared to December 2024, and a 19.1% decline year-on-year.

For more information, please click on:

International Statistical Cooperation

|

International Statistical Cooperation

|

Statistical Literacy

|

Statistical Literacy

|

|

|

|

|

|

|

Copyright © 2026 Direção Regional de Estatística da Madeira. All rights reserved.

Address: Calçada de Santa Clara 38, 9004-545 Funchal, Madeira Island

Phone: +351 291 145 126 (National landline call)